If you’re searching for clarity on asia-pacific central bank rate decisions, you’re likely trying to understand how shifting monetary policies across the region will affect currencies, equities, trade flows, and your broader investment strategy. With inflation pressures, growth slowdowns, and global rate divergence reshaping markets, even a single basis-point move can ripple across the Asia-Pacific economy.

This article breaks down the latest rate announcements, the policy signals behind them, and what they mean for businesses, investors, and policymakers. We analyze official central bank statements, macroeconomic data releases, and regional market reactions to separate meaningful policy shifts from short-term noise. By grounding our insights in verified data, historical rate cycles, and cross-border economic linkages, we provide a clear, forward-looking view of how monetary tightening, easing, or pauses could influence capital flows, trade balances, and financial stability across the region.

Whether you’re tracking currency volatility or long-term growth prospects, this guide delivers focused, data-driven insight into what matters now.

The Policy Split

Navigating today’s Asia-Pacific economy means understanding why central banks are no longer synchronized. This year’s asia-pacific central bank rate decisions reflect different inflation paths, growth pressures, and currency risks. Japan’s gradual tightening contrasts with China’s targeted easing, while Australia stays data-dependent.

Investors often ask: what does this mean for portfolios? Divergence typically drives currency volatility and reshapes capital flows, especially in trade-heavy economies.

- Watch interest differentials; they influence carry trades and export competitiveness.

Some argue policy gaps create opportunity. True, but they also amplify hedging costs and planning uncertainty. Focus on inflation trends and forward guidance carefully.

Inflation vs. Growth: The Core Tension Driving Rate Decisions

The Global Context

Lingering global inflation hasn’t faded as quickly as many hoped (remember the “transitory” debate?). The US Federal Reserve’s higher-for-longer stance keeps global liquidity tight, effectively setting a floor under borrowing costs worldwide. When the Fed holds firm, capital often flows back to dollar assets, pressuring Asia-Pacific currencies and forcing difficult asia-pacific central bank rate decisions. In my view, even economies with mild inflation feel compelled to signal discipline just to avoid currency volatility.

The Regional Split

The divide is stark. Australia and the Philippines have leaned hawkish, prioritizing inflation control as consumer prices strain households. Meanwhile, China and Vietnam tilt dovish, favoring stimulus to revive growth and property markets. I think both camps have valid logic—but growth-first strategies risk reigniting price pressures if stimulus overshoots (a policy déjà vu we’ve seen before).

Domestic Factors at Play

Internal dynamics matter just as much:

- Domestic consumption resilience

- Real estate market stability

- Government debt servicing costs

High rates cool inflation, but they also squeeze borrowers and public finances. That trade-off is unavoidable.

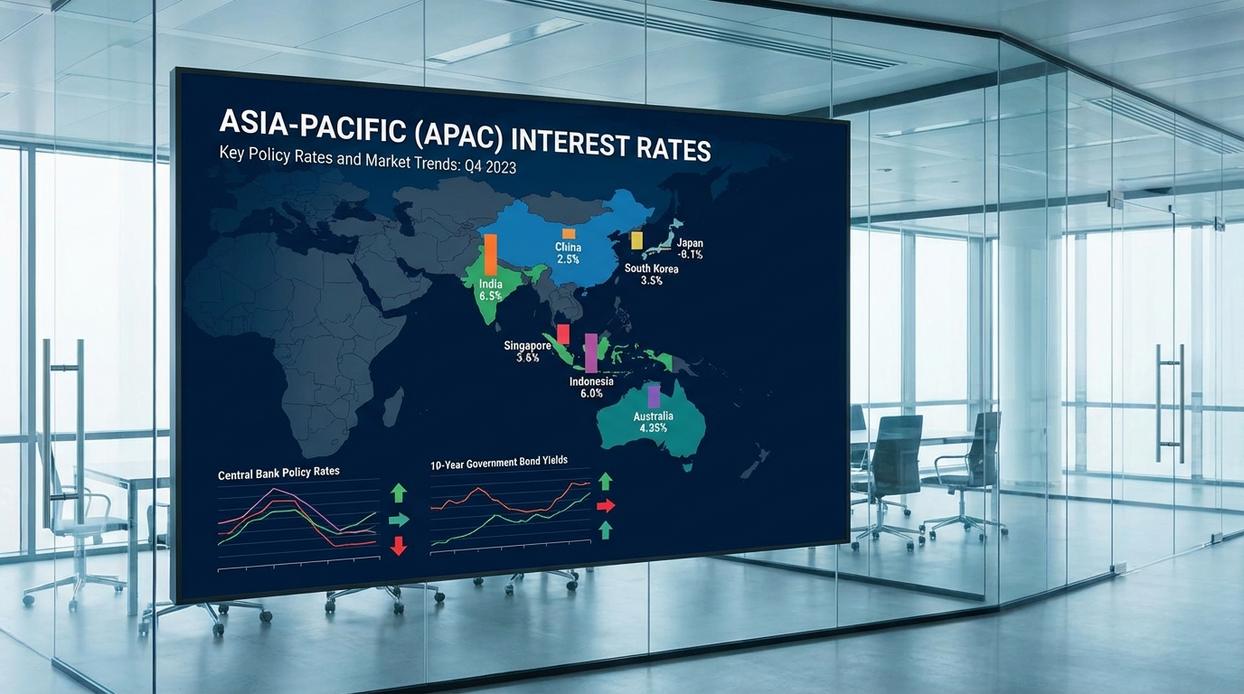

Latest Policy Rates (approx.):

- RBA (Australia): 4.35%

- BOJ (Japan): ~0.10%

- PBoC (China LPR): 3.45%

- RBI (India): 6.50%

Personally, I believe 2026 will test who balanced credibility with flexibility best.

Case Study 1: Bank of Japan’s Historic Pivot and Its Ripple Effects

When the Bank of Japan finally ended its negative interest rate policy in 2024, markets blinked twice. After years of ultra-loose monetary policy—where rates sat below zero to stimulate borrowing—the shift felt almost surreal. Why now? Core inflation holding above the BOJ’s 2% target and steady wage growth signaled that Japan might finally be escaping decades of deflation (a persistent decline in prices). Have you ever wondered what happens when a country rewrites a policy playbook it’s used for years?

The immediate impact on the yen (JPY) was volatility. As a funding currency—meaning investors borrow it cheaply to invest elsewhere—the yen had long powered global carry trades. With rates rising, that trade becomes less attractive. Could the yen strengthen long term? Possibly, especially as asia-pacific central bank rate decisions increasingly diverge.

For investors, the ripple effects are complex:

- CAPS SHIFT IN POLICY EXPECTATIONS

- Rising yields pressure Japanese government bonds (JGBs)

- A stronger yen may weigh on export-heavy Nikkei firms

Some argue Japan’s tightening will be gradual and symbolic. But even symbolic pivots can reset foreign investment flows. Are portfolios positioned for that reality?

Case Study 2: Southeast Asia’s Balancing Act

The ASEAN Bloc

Southeast Asia isn’t a monolith (despite what headline writers suggest). Within ASEAN, policy paths diverge sharply. Indonesia has prioritized Rupiah stability, intervening in currency markets and holding rates relatively firm to anchor investor confidence. A stable currency, after all, keeps imported inflation in check and reassures bond markets. Thailand, by contrast, has leaned toward stimulating tourism and domestic demand—accepting softer currency pressures to revive growth after pandemic-era scarring.

Critics argue both strategies are risky. Some say Indonesia’s tight stance restrains credit and slows SMEs. Others warn Thailand’s accommodative tilt could fuel asset bubbles. Both points have merit. But in practice, each central bank is responding to its dominant vulnerability: capital outflows for Indonesia, weak consumption for Thailand.

Trade Agreement Impact

RCEP, the Regional Comprehensive Economic Partnership, reduces tariffs across member states. In theory, that should encourage coordination. In reality, countries still compete for export advantages. Divergent rate paths—visible in recent asia-pacific central bank rate decisions—reflect this tension. (Free trade doesn’t mean uniform policy.) For deeper context, see quantitative tightening trends among apac economies.

Future Outlook

Next quarter, Indonesia is likely to hold, prioritizing currency defense. Thailand may cut modestly if tourism inflows soften. Vietnam, facing cooling exports, could ease selectively. Pro tip: watch core inflation, not just headline CPI—it often signals the real pivot point.

Translating Policy to Portfolio: Impact on Trade and Investment

Interest rates don’t just move charts—they move capital. And in Asia-Pacific, those shifts ripple quickly through currencies, foreign direct investment (FDI), and supply chains.

Currency and Forex Markets

When interest rate differentials (the gap between two countries’ benchmark rates) widen, currency pairs like AUD/JPY and USD/SGD react fast. For example, if Australia raises rates while Japan holds steady, yield-seeking investors often favor the Australian dollar. As a result, AUD/JPY may strengthen.

Practical tip: Compare central bank rate paths before entering a trade. Then, confirm with inflation data and forward guidance. This reduces the risk of chasing short-term volatility (which can reverse quickly).

That said, critics argue forex markets already price in rate decisions. Fair point. However, surprises—especially around asia-pacific central bank rate decisions—still trigger sharp repricing, creating tactical entry points.

Foreign Direct Investment (FDI)

Higher rates can signal stability—or raise borrowing costs. For manufacturing and tech investors, a stable currency often outweighs slightly higher financing costs. For instance, a firm choosing between Vietnam and another market may prioritize predictable exchange rates over marginally cheaper loans.

Supply Chain Dynamics

Meanwhile, a weaker local currency lowers export prices but raises import costs. If you source components internationally, hedge currency exposure before signing long-term contracts. In practice, even a 3–5% currency swing can materially alter margins.

Strategic positioning in APAC demands clarity, not guesswork. We now understand why central banks are diverging, but the real test is acting amid uncertainty. In my view, investors overcomplicate asia-pacific central bank rate decisions when the answer is simpler: follow domestic priorities. Is inflation sticky? Is growth stalling? Is currency stability under threat? Those signals matter MORE than headlines. Watch CPI, GDP, and PMI for early clues about the next pivot. I believe DISCIPLINE, not drama, wins in this cycle. React to data, not noise, and you will stay positioned for the region’s next policy wave. Stay ALERT. That’s essential.

Stay Ahead of Asia’s Shifting Economic Forces

You came here to better understand the forces shaping Asia’s economic direction — from market momentum to policy signals and cross-border trade dynamics. Now you have a clearer view of how asia-pacific central bank rate decisions influence liquidity, currency stability, investment flows, and business confidence across the region.

In today’s environment, the real risk isn’t volatility — it’s being unprepared for it. Rate shifts, policy adjustments, and trade developments can quickly reshape opportunity and exposure. Staying informed isn’t optional; it’s your competitive edge.

If you want sharper insights, timely forecasts, and clear analysis that helps you anticipate what’s next instead of reacting too late, now is the time to act. Follow our latest Horizon Headlines, monitor upcoming policy announcements, and leverage our Asia-Pacific economic outlook reports to guide your strategy.

Don’t let sudden policy moves catch you off guard. Stay informed, stay prepared, and position yourself ahead of the next market shift.